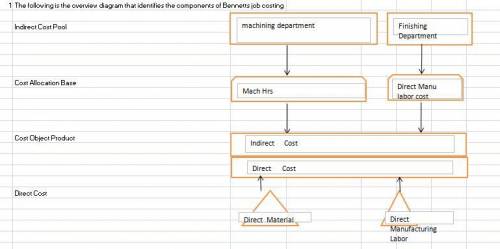

WoolCorp

1. Single Plantwide Factory Overhead Rate: $652

2. Comparison of WoolCorp’s current method with activity-based costing:

Raw Wool Wool Yarn

Allocated factory

overhead cost $45,640 $19,560

Activity-Based Costing $17,840 $47,640

3. Calculation of and entering the activity rate for each of the three activities:

Activity Activity Rate

Sorting $6.40 ($25,600/4,000)

Cleaning $6.00 ($38,400/6,400)

Combing $12.00 $1,200/100)

4. Allocation of the costs of sorting, cleaning, and combing to product:

Raw Wool Wool Yarn

Sorting cost $5,120 $20,400

Cleaning cost 11,520 26,880

Combing cost 840 360

Total cost $17,840 $47,640

5. Recommended method of costing:

Activity-based costing, because it recognizes differences in how each product uses factory overhead activities, yielding more accurate product costs.

Explanation:

Key Decisions: product offerings, pricing, and vendors

Problem: method of assigning overhead to products

Products:

(1) raw, clean wool to be used as stuffing or insulation and

(2) wool yarn for use in the textile industry

Requirement: evaluate its costing methods for its raw wool and wool yarn.

Traditional Costing Method : Predetermined overhead rate computed as follows:

Single Plantwide Factory Overhead Rate= (Total Budgeted Factory Overhead) ÷ (Total Budgeted Plantwide Allocation Base) combing machine hours

Data for the production of 550 pounds of either raw wool or wool yarn:

Factory Overhead Type Budgeted Factory Overhead

Sorting $25,600

Cleaning $38,400

Combing $1,200

Total overhead $65,200

Raw Wool Wool Yarn

Hours of combing

machine use required 70 30

Compiled Information:

Type of Cost Activity Base Total Cost Rate

Sorting Hours of sorting $25,600

Cleaning Units of cleaning

machine power $38,400

Combing Hours of combing

machine use $1,200

Raw Wool Wool Yarn Total

Hours of sorting required 800 3,200 4,000

Units of cleaning machine

power required 1,920 4,480 6,400

Hours of combing

machine use required 70 30 100

1

1